In Your Best Interest

Or, How to make sure that your money is ACTUALLY working for you

… and for those who prefer to hear words rather than read them, I’ve put together a talkie just for you!

My wife and I sit down with our financial advisor once a quarter and walk through a version of this sheet, talking about where we are, what is changing, any moves we plan to make and how we might better allocate our funds to maximize our future growth. The value of these conversations and the guidance of a financial professional cannot be understated.

There are a lot of programs that can track your spending and help you build a balance sheet that can give you a snapshot of your financial picture, from a simple spreadsheet to newer AI-powered apps. (I use Tiller Money connected to Google Sheets. Please avoid Rocket Money, it’s just a lead funnel for their mortgage division). The problem is just that a snapshot is static, two-dimensional, and doesn’t give insight as to:

How assets are growing (or not)

What liabilities are costing you

The opportunity costs of where your money could be located

To see these, you need some special decoder glasses to add a third dimension to your data.

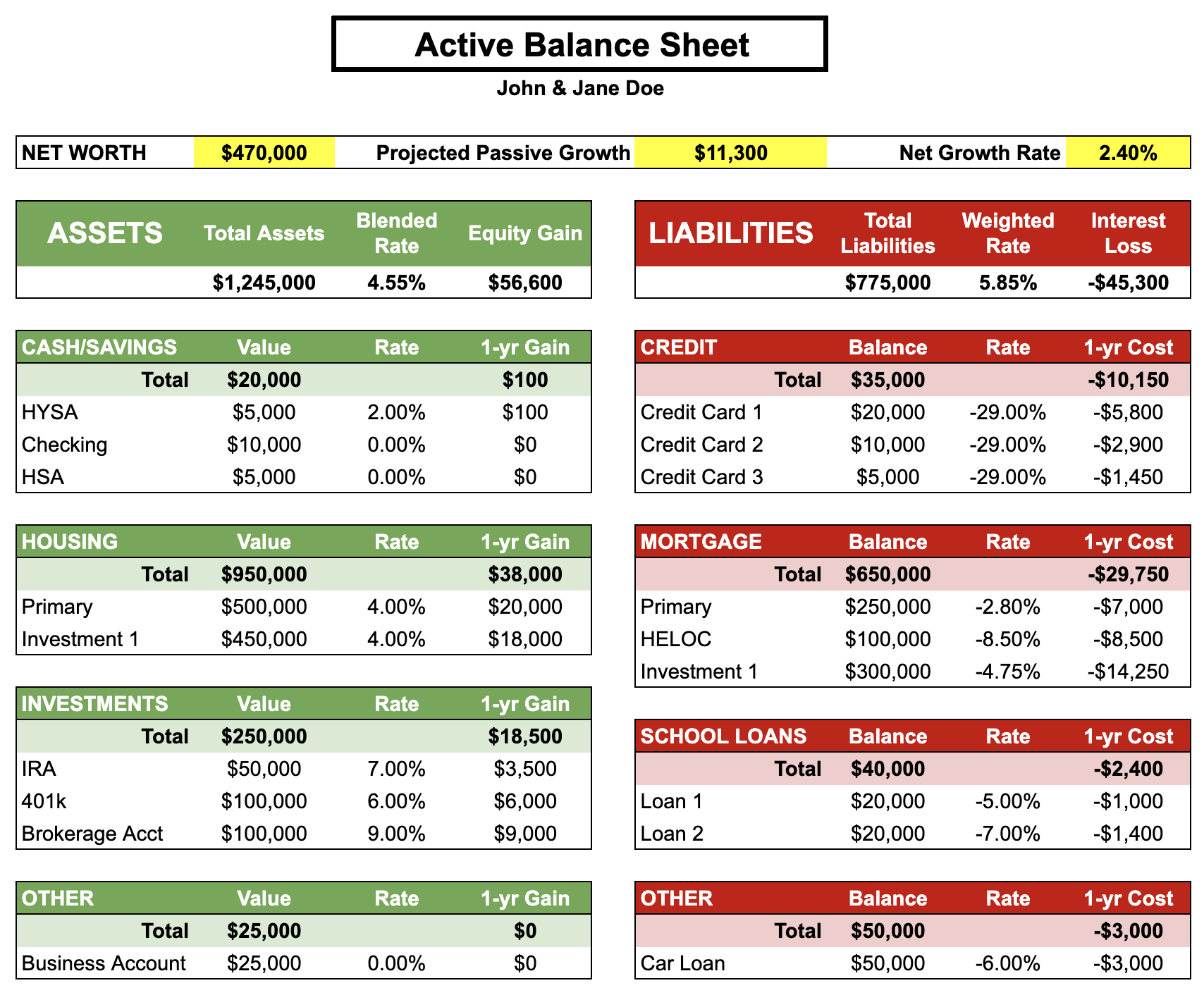

The Active Balance Sheet

The goal of this sheet is to change the question from: ‘How much do I have?’ to ‘What is my money doing?’

To do this, I’ve added the dimension of interest rate and expected growth, to allow you to see how a year in those accounts will affect your overall Net Worth.

Here is a simplified example for John and Jane Doe. They are a couple in their late 30’s with a primary residence and a rental property that used to be their first home. They have some money in retirement and brokerage accounts, carry some lingering student loans, a car loan (for the new hybrid minivan), and bit too much credit-card-debt. In other words, they’re a typical upwardly-mobile couple that has made some good moves and is looking to grow their wealth faster.

A few notes on the figures here:

The interest rates on the Liability side of the ledger are pretty easy to calculate because they’re shown on any account statement.

The rates on the Asset side are often harder to crystallize, because they are projections of growth over the next year based on historical performance.

The average appreciation of single-family real estate in the NW over the last 60 years has been about 4.5%, buoyed by our inability to build housing to meet demand.

In this case, the Doe’s are growing their net worth passively by $11k per year, or at a 2.4% annual rate. That is a decent pace, depending their other spending habits, but there are a few pieces of advice that I would give them to push that number even higher:

High-interest debt is a killer

The first move to prioritize would be to eliminate the credit card debt, which is costing them $10k each year just in interest, which cancels out almost 20% of their gains. High CC debt is often a sign of a household spending more than they are bringing in on a monthly basis (or possibly going through a job loss, or other loss of income). However quickly they can (including draining their savings down to a three-month cushion), the number 1 goal is to remove high-interest debt and keep it down. We do a lot of debt-consolidation loans that can help get your debt from ridiculous to manageable rates to help quicken up paydown.

Cash is important, but only to a point

Cash may be king, but it’s king of a tiny realm. Having a 3-6 month spending cushion in savings or other liquid account is an important early step toward financial health, but holding beyond that is inefficient. If it is not earning more than 3%, it is losing spending power to inflation. Once debt is paid down, put cash to work for you.

Size matters

Net worth is driven more by the size of the assets you control than the rate you are earning. For the Doe’s, their brokerage account earns a 9% annual return, and the investment property only 4% appreciation per year. But in real returns, the investment property is double because it’s valued at $450k rather than $100k.

Even the 4% appreciation figure is misleading. While the market will push the top-line value up at 4% annually, the Doe’s bought the house using a mortgage. If the balance of that loan is $300k, that means that their equity is $150k and they are leveraging the house at a 3:1 ratio, which makes the $18k annual appreciation a 12% return on their equity. It’s the power of real estate!

Money moves

Your balance sheet is constantly changing, and should be revisited regularly to ensure that your resources are allocated in the smartest places. Every financial decision is a reallocation:

Buying a home reduces Cash, increases Real Estate and adds a Mortgage liability

Renovating a property with a HELOC will add or increase a Mortgage liability, but will increase the value of the Real Estate

Putting money where it can do the most good (either utilizing high-return accounts or leveraging into real estate) is the name of the game to maximize the growth rate of your Net Worth.

Compounding works on both sides

Over time, the assets will appreciate while the associated debts decreases at an accelerating rate (for fixed-rate debts). The longer the flywheel turns, the more momentum it builds, until the equity in those assets can be harvested to acquire more or bigger assets!

Negative decisions can compound, too. If high-interest debt is poorly used, or cash isn’t working efficiently, the opportunity costs add up as well.

Yeahbut…

One big constraint to building wealth with this mindset is liquidity. You can’t eat your house, so making sure that you have enough liquid assets to handle a downturn, emergency or a project running long. If you don’t have spare cash to buffet any negative events, you may be in a fragile position. It is important to increase your liquidity as your portfolio grows to allow you to make bigger investments and keep steady when all is not right with the world. Resiliency is important, because selling assets in a panicked state will lead to losing a lot of hard-earned, hard-fought equity.

You can access a copy of the Active Balance Sheet here and try it with your own numbers. I’d love to hear what you learn through the process! If you want help visualizing your own position, I’d love to be of help.